Inflation Steady, Home Sales Show Momentum!

Week of September 22, 2025 in Review

The Fed’s go-to inflation gauge came in as expected, jobless claims highlight ongoing hurdles for workers, and home sales are beginning to reflect the recent dip in mortgage rates. Read on for more key takeaways.

- Fed’s Key Inflation Gauge Holds Steady

- Initial Jobless Claims Decline Again

- August Existing Home Sales Edge Lower

- New Home Sales Surge

- Q2 GDP Beats Expectations

- Family Hack of the Week

- What to Look for This Week

- Technical Picture

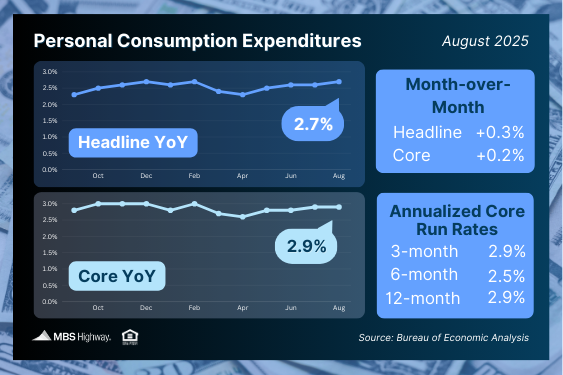

Fed’s Key Inflation Gauge Holds Steady

August’s inflation report came in largely as expected. The Personal Consumption Expenditures (PCE) index showed a 0.3% monthly rise in overall inflation, nudging the annual rate from 2.6% to 2.7%.

Core PCE – the Fed’s preferred inflation gauge, which strips out food and energy – rose 0.2% for the month and remained steady at 2.9% year-over-year.

What’s the bottom line? The Fed is caught between two competing forces: inflation that’s still above target and growing signs of economic softening. That push-and-pull was evident in the September 17 rate cut, where the Fed pointed to “rising downside risks to employment.” The next few labor reports – especially the September Jobs Report due October 3 – will be crucial in shaping what comes next at the Fed’s October 29 meeting.

Quick refresher: When the Fed changes interest rates, it’s adjusting the Fed Funds Rate – the short-term rate banks use to lend to each other. While this doesn’t directly set mortgage rates, it does influence them, along with other economic factors.

Initial Jobless Claims Decline Again

Initial jobless claims fell to 218,000, marking the second consecutive weekly drop after hitting a four-year high. Continuing claims, representing those still receiving unemployment benefits, also edged down by 2,000 to 1.926 million.

What’s the bottom line? While the drop in new claims is encouraging, continuing claims have held above 1.9 million for 18 consecutive weeks. This suggests it’s taking longer for people to find new jobs – an indication of a cooling labor market.

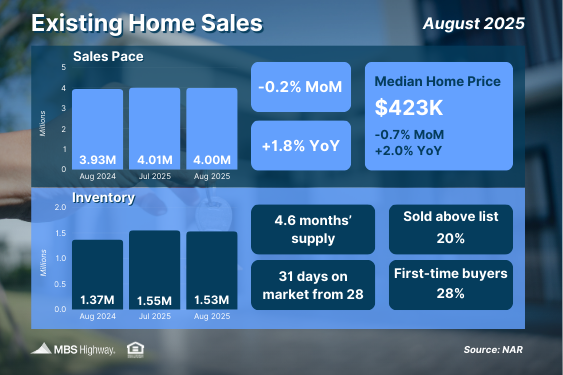

August Existing Home Sales Edge Lower

Existing home sales were nearly flat from July to August, slipping just 0.2% to a 4 million annual pace, according to the National Association of REALTORS® (NAR). Inventory also declined slightly from July, but the 1.53 million homes on the market marked an 11.7% increase from a year ago.

What’s the bottom line? This report reflects closings in August, meaning most buyers were shopping in June and July before mortgage rates began to ease. According to NAR Chief Economist Lawrence Yun, lower rates and higher inventory should help support stronger sales in the coming months.

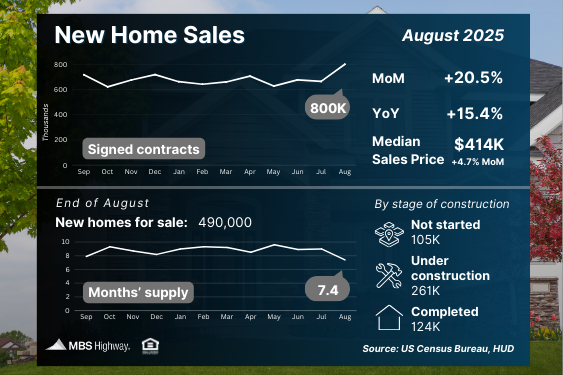

New Home Sales Surge

New home sales jumped nearly 21% month-over-month in August, reaching an annualized pace of 800,000 units – the fastest rate since early 2022 and well above economists’ expectations. The data reflects contracts signed during August, when rates had already started trending lower from July, though still ahead of the larger declines seen in September.

Adding to the momentum, July’s sales were revised upward from 652,000 to 664,000.

What’s the bottom line? Sales are expected to remain strong in the coming months as lower mortgage rates help improve affordability.

However, the supply of move-in ready homes remains tight. At the end of August, there were 490,000 new homes on the market – one of the highest totals since 2007. Yet only 124,000 of those were completed and available for immediate occupancy. The rest were still under construction or not yet started, underscoring the continued need for more finished homes to meet rising demand.

Q2 GDP Beats Expectations

The final estimate for second quarter 2025 GDP shows the U.S. economy grew by 3.8%, up from the previous estimate of 3.3%.

What’s the bottom line? GDP is a key measure of economic health, and this strong Q2 growth marks a sharp rebound from the 0.6% decline in Q1. That earlier drop was largely driven by a spike in imports as businesses rushed to stock up ahead of potential tariffs. Since imports subtract from GDP, fewer imports in Q2 helped boost the number – along with a pickup in consumer spending.

For the first half of the year, the economy is averaging 1.6% growth.

Family Hack of the Week

Celebrate National Biscotti Day on September 29 – or enjoy a treat anytime – with these crunchy, delicious Pistachio Biscotti from Food Network. This easy recipe makes 24 cookies.

Start by toasting 1 1/2 cups of pistachios on a cookie sheet in a 350 degree Fahrenheit oven for about 10 minutes, then set aside. In a mixer, beat 1/2 cup of unsalted butter until fluffy, then mix in 3 eggs, 1 cup sugar, and 1 teaspoon vanilla until smooth. Add 3 1/2 cups of flour, 1 teaspoon of baking powder, and 1/2 teaspoon of salt. Once the dough comes together, stir in the pistachios.

Divide the dough in half and shape into two 12-inch-long logs. Place them on an ungreased cookie sheet and bake for about 35 minutes, until lightly browned. Let cool for 5 minutes, then slice each log diagonally into 12 1-inch-thick pieces. Return the slices to the cookie sheet and bake for 5 minutes per side to crisp. Cool completely and store in an airtight container.

What to Look for This Week

The week begins with key housing data: Pending Home Sales on Monday, followed by home price appreciation reports on Tuesday.

Labor market data also kicks off Tuesday with August’s Job Openings and Labor Turnover Survey (JOLTS). On Wednesday, we’ll get ADP’s private payroll report for September, followed by weekly jobless claims on Thursday. The week concludes Friday with the closely watched September employment report from the Bureau of Labor Statistics, which includes non-farm payrolls and the unemployment rate.

Technical Picture

Mortgage Bonds tested resistance at their 25-day Moving Average last Friday but ultimately closed below it. There’s now plenty of room to the downside before the next support level at the 50-day Moving Average.

Meanwhile, the 10-year Treasury yield challenged support at its own 25-day Moving Average, which held – pushing yields higher by week’s end. There’s still room for yields to rise before they reach the next resistance at the 50-day Moving Average.